Tax Free Savings Account (TFSA) came into affect in January 2009. There are tax benefits to using the TFSA as a short-term savings plan; however, these benefits can be much greater if the TFSA is used as a long-term investment plan. Why? It’s all about the power of tax-free compound growth.

Plan overview:

Q: What is the Tax-Free Savings Account (TFSA)?

A: The TFSA is a flexible, registered general-purpose account that will allow Canadians to earn tax-free investment income. TFSA is most effective when used as a long-term investment account because investors will benefit from tax-free compound growth.

Q: Who can invest in a TFSA?

A: In order to be eligible to invest in a TFSA, an individual must:

- Be 18 years of age or older;

- Be a Canadian resident taxpayer;

- and Have a valid social insurance number.

Q: How much can I contribute to my TFSA?

TFSA contribution room is based on an individual’s allocated annual TFSA amount and their unused TFSA carryforward amount. The annual allocated dollar amount is indexed to inflation and rounded to the nearest $500. From 2009 to 2012 the annual TFSA contribution limit was $5,000. In 2013, due to indexation, the annual allocated dollar amount was increased to $5,500.

Q: When does TFSA contribution begin to accumulate?

A: TFSA contribution room will begin to accumulate in any year after 2009, provided the individual is a Canadian resident and at least 18 years of age in the year.

Q: How does carryforward of unused contribution room work?

A: An investor can calculate TFSA contribution room at the beginning of each calendar year. The calculation considers the investor’s unused TFSA contribution room at the end of the preceding calendar year, plus any TFSA withdrawals made in that year. That figure is added to the TFSA dollar limit for the current year minus all contributions made in the current year.

Note that certain qualifying transfers and prescribed withdrawals are excluded from the calculation.

Q: How much can be redeemed tax-free from a TFSA?

A: You can redeem the entire value of the TFSA without paying tax on the investment income.

Q: Are contributions into a TFSA tax-deductible?

A: No.

Q: Do withdrawals have an impact on my contribution room?

A: Yes. If a withdrawal is made from a TFSA in a year, the amount withdrawn is added to the individual’s TFSA contribution room calculation for the next year and can be re-contributed in subsequent years.

Q: What happens if I overcontribute to my TFSA?

A: Any excess contribution will be subject to a 1% penalty tax per month.

Q: Can I name a beneficiary or successor account holder directly on the TFSA plan?

A: Yes, beneficiary and successor accountholder designations may be made directly on the TFSA plan unless you are a resident of Quebec .

Q: Is the interest expense incurred on money borrowed to invest in a TFSA plan tax-deductible?

A: No.

Q: Can I use my TFSA as collateral for a loan?

A: Yes, this is specifically authorized and will have no negative tax consequences.

Q: Can I contribute to my TFSA as a non-resident of Canada?

A: While there is nothing preventing a TFSA account holder from contributing to a TFSA while being a non-resident of Canada, any contributions made during non- residency will be subject to a 1% penalty per month for each month these funds remain in the plan. Also, the annual TFSA dollar amount will not be allocated during years of non-residence.

Q: Can anyone else make contributions into my TFSA?

A: No. Contributions can only come from the account holder.

Q: Can I hold a TFSA in joint ownership with my spouse or adult children?

A: No.

Q: Can I open a TFSA in-trust for my minor children?

A: No.

Q: What happens to the TFSA upon death of the account holder?

A: The full account value becomes an asset of the account holder’s estate. While no tax is incurred on passing into the estate, any income after death will be taxable. However, if there is a surviving spouse who is named as successor holder, that spouse may maintain that account as a TFSA, without any reduction in the spouse’s contribution room.

Q: What would happen to a TFSA in the event a marriage or common-law partnership is dissolved?

A: A transfer could be made directly from one spouse or common-law partner’s (former spouse or common-law partner) TFSA to the other without any taxable situation. The amount of the transfer would not affect either spouse’s or common-law partner’s TFSA contribution room.

Q: How is a TFSA different from an RRSP?

A: An RRSP is primarily intended for retirement. The TFSA can be used for pre-retirement, retirement and estate-planning goals. Both plans offer tax advantages, but they have key differences.

- RRSP contributions are deductible from income

- Although growth and income generated in an RRSP plan is not taxable, withdrawals from the plan are taxable except in certain circumstances

- TFSA contributions are not tax-deductible, are likewise not taxed on any income generated in the plan and are completely tax-free on withdrawal

- Withdrawals from an RRSP or RRIF may affect other senior benefits such as Old Age Security (OAS) and the Guaranteed Income Supplement (GIS), whereas withdrawals from a TFSA will not

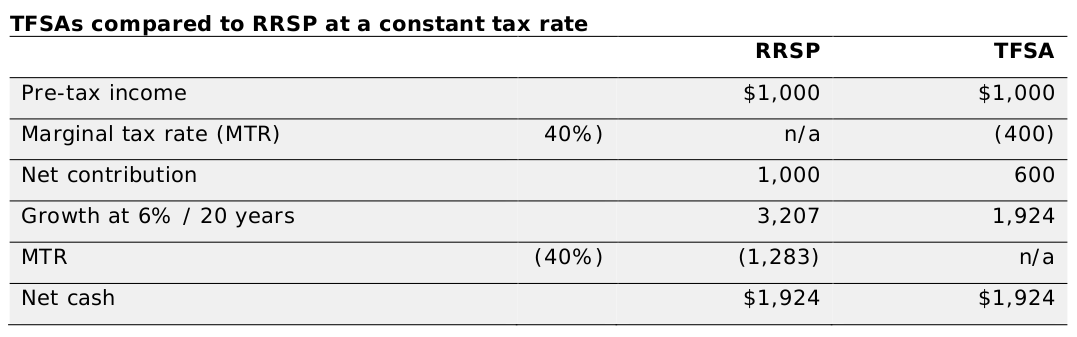

Q: Should I make a contribution to my RRSP or my TFSA this year? Which one should I maximize first if I don’t have enough extra cash to contribute to both?

A: While the plans are meant to be tax-neutral where a person has the same marginal tax rate at all times (see chart below), RRSPs will tend to make more sense when the tax rate upon withdrawal is expected to be lower than your tax rate upon original contribution. Conversely, TFSAs will work out better if your tax rate (including the effect of RRSP withdrawals on reduced income-tested benefits) will be higher upon ultimate withdrawal than it was when you contributed.